Depreciation Calculator: The Tax Deduction Most Businesses Get Wrong

5 Methods Covered

Straight-line, declining balance, double-declining, sum-of-years, and MACRS

Tax Impact Built In

See year-by-year tax savings at your marginal rate

IRS MACRS Tables

Official GDS percentages for 3- through 39-year property classes

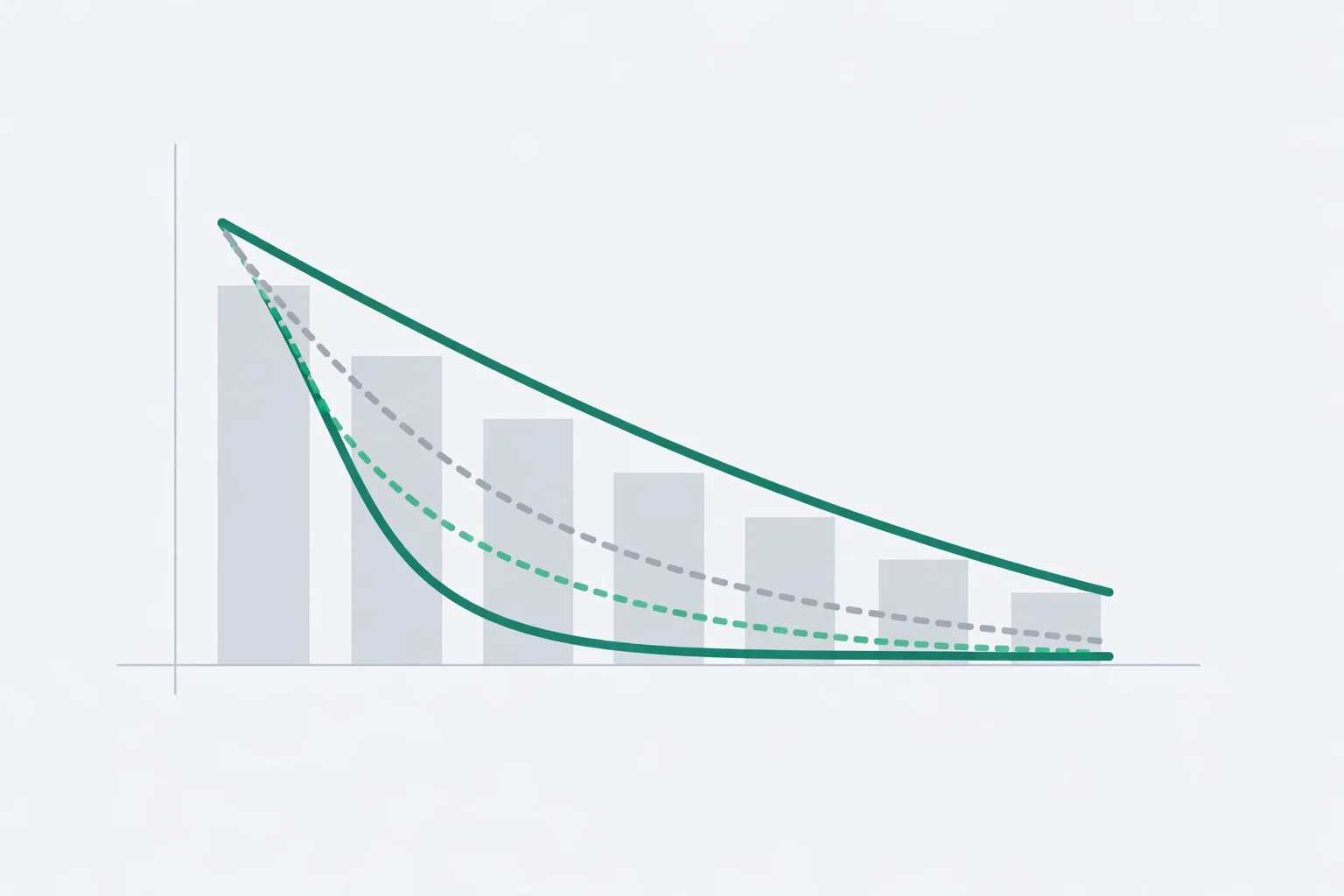

A depreciation calculator helps you figure out how much of an asset's cost you can deduct each year — but most business owners pick the wrong method and leave thousands on the table. A company that buys a $50,000 delivery van and defaults to straight-line depreciation over 7 years claims $6,429 in Year 1. Switch to MACRS 5-year property and that same van generates a $10,000 first-year deduction — 56% more. Over five years, the timing difference shifts roughly $3,750 in tax savings earlier, money that compounds or covers cash flow gaps instead of sitting with the IRS.

The misconception is that depreciation methods all produce the same total deduction. They do — eventually. But when you take those deductions matters enormously for cash flow, and the IRS doesn't require you to use the slowest method available.

Straight-Line: Simple but Often Suboptimal

Straight-line depreciation divides the depreciable basis evenly across the asset's useful life. The formula is straightforward:

For a $50,000 asset with a $5,000 salvage value and 7-year life, that's ($50,000 − $5,000) ÷ 7 = $6,429 per year, every year, for seven years. The book value drops in a perfectly straight line from $50,000 to $5,000.

Straight-line works well for assets that genuinely lose value at a steady rate — commercial buildings, long-lived equipment, or intangible assets like patents. It's also the only method allowed under GAAP for most financial reporting. But for tax purposes, you almost always have a better option. If you're calculating the cost basis for a property transaction, our cost basis calculator handles those adjustments.

How Accelerated Methods Front-Load Your Deductions

Accelerated depreciation recognizes a simple economic truth: most assets lose more value in their early years. A new laptop depreciates faster in year one than year five. Accelerated methods match that reality and, more importantly, put tax deductions in your hands sooner.

Double-Declining Balance (DDB)

DDB applies twice the straight-line rate to the remaining book value each year. For a 7-year asset, the straight-line rate is 14.29%, so DDB uses 28.57%.

Year 1: $50,000 × 28.57% = $14,286. Year 2: $35,714 × 28.57% = $10,204. By mid-life, annual depreciation has already dropped below the straight-line amount. DDB never depreciates below salvage value — when the book value approaches it, the deduction tapers to zero.

Sum-of-the-Years' Digits (SYD)

SYD creates a declining fraction for each year. For a 7-year asset, the sum of digits 1+2+3+4+5+6+7 = 28. Year 1 gets 7/28 of the depreciable basis, Year 2 gets 6/28, and so on. On our $45,000 depreciable basis: Year 1 = $45,000 × 7/28 = $11,250. Year 7 = $45,000 × 1/28 = $1,607. SYD is smoother than DDB but still front-loaded.

| Year | Straight-Line | Double-Declining | Sum-of-Years | MACRS 7-Year |

|---|---|---|---|---|

| 1 | $6,429 | $14,286 | $11,250 | $7,145 |

| 2 | $6,429 | $10,204 | $9,643 | $12,245 |

| 3 | $6,429 | $7,289 | $8,036 | $8,745 |

| 4 | $6,429 | $5,207 | $6,429 | $6,245 |

| 5 | $6,429 | $3,719 | $4,821 | $4,465 |

| 6 | $6,429 | $2,656 | $3,214 | $4,460 |

| 7 | $6,429 | $1,639 | $1,607 | $4,465 |

| 8 | — | — | — | $2,230 |

| Total | $45,000 | $45,000 | $45,000 | $50,000 |

Based on $50,000 asset, $5,000 salvage value, 7-year life. MACRS uses full cost basis (no salvage value).

Notice that MACRS depreciates the full $50,000— not $45,000 — because it ignores salvage value. That's an extra $5,000 in total deductions the other methods don't give you.

MACRS: What the IRS Actually Expects You to Use

The Modified Accelerated Cost Recovery System isn't optional for most business property. The IRS requires MACRS for tangible property placed in service after 1986. It uses prescribed recovery periods (3, 5, 7, 10, 15, 20, 27.5, or 39 years) with built-in half-year conventions. You don't estimate useful life — the IRS tells you.

| Property Class | Common Assets | Year 1 Rate | Total Years |

|---|---|---|---|

| 3-Year | Tractors, specialized small tools | 33.33% | 4 |

| 5-Year | Cars, trucks, computers, copiers | 20.00% | 6 |

| 7-Year | Office furniture, fixtures, most equipment | 14.29% | 8 |

| 15-Year | Land improvements, parking lots, fences | 5.00% | 16 |

| 27.5-Year | Residential rental buildings | 3.636% | 28 |

| 39-Year | Commercial buildings, office space | 2.461% | 40 |

MACRS GDS rates using the half-year convention (IRS Publication 946). "Total Years" includes the partial final year.

The key detail most people miss: MACRS 5-year property actually takes 6 calendar years to fully depreciate because of the half-year convention — you only get half a year's worth of depreciation in both the first and last years. A $50,000 computer system placed in service in July still gets 20% ($10,000) in Year 1, the same as one placed in January. If you own rental property, our rental yield calculator can help you see how depreciation affects your net returns.

The $12,500 Mistake: Choosing the Wrong Recovery Period

Classifying a 5-year asset as 7-year costs you real money

A $50,000 asset in the 5-year class generates $10,000 in Year 1 deductions. The same asset wrongly classified as 7-year property yields only $7,145 — a $2,855 difference. At a 25% tax rate, that's $714 less in your pocket in Year 1 alone. Over the full recovery period, the timing mismatch costs about $1,200-$1,800 in present-value terms at a 5% discount rate.

Forgetting to separate land from building cost

Land is never depreciable. If you buy a $500,000 commercial property and 20% ($100,000) is land value, your depreciable basis is $400,000 — not $500,000. Depreciating the full $500,000 creates a $100,000 over-deduction that triggers penalties and interest when the IRS catches it during an audit.

Using book depreciation for tax returns (or vice versa)

GAAP financial statements use straight-line. Your tax return uses MACRS. They're two parallel systems with different numbers. Mixing them up means either overpaying taxes or triggering an audit. Track both separately.

Section 179 and Bonus Depreciation: The Accelerators on Top of MACRS

MACRS isn't the fastest way to deduct an asset. Section 179 lets you expense the entire cost of qualifying equipment in the year you place it in service — up to $1,220,000 for 2024 (the limit adjusts annually for inflation). Bonus depreciation, currently at 60% for 2024 and phasing down 20% per year, applies to the remaining balance after Section 179.

Here's what this looks like on a $150,000 piece of manufacturing equipment:

| Strategy | Year 1 Deduction | Tax Savings (25%) | Remaining Basis |

|---|---|---|---|

| MACRS 7-Year Only | $21,435 | $5,359 | $128,565 |

| Bonus (60%) + MACRS | $98,574 | $24,644 | $51,426 |

| Section 179 (Full) | $150,000 | $37,500 | $0 |

Section 179 subject to taxable income limits. Bonus depreciation phasing down from 80% (2023) to 0% (2027).

The catch: Section 179 deductions can't exceed your taxable business income for the year. If your business earns $120,000, you can only deduct $120,000 under Section 179 — the remaining $30,000 carries forward. Bonus depreciation has no income limit, which is why many businesses use a combination of both. For a broader view of how equipment costs affect your business finances, our business loan calculator can model financing scenarios alongside depreciation.

When Straight-Line Actually Wins

Accelerated depreciation isn't always the right call. Here are three situations where straight-line is the better strategy:

You expect higher income in future years

If your tax rate will be higher in 3 years (new contracts, business growth), saving deductions for those years produces bigger savings. A $6,429 deduction at 32% saves $2,057 vs. $1,607 at 25%.

The asset holds value steadily

Commercial buildings, infrastructure, and some industrial equipment depreciate at roughly constant rates. Straight-line matches economic reality and simplifies bookkeeping.

You're in a low-income year with carryforward limits

Startup years with minimal revenue mean big deductions just create NOL carryforwards. In some cases, spreading deductions evenly produces better cash-flow timing.

A Real Depreciation Decision: Delivery Fleet Example

A logistics company buys 5 delivery vans at $45,000 each — $225,000 total. Vehicles are MACRS 5-year property. Here's the year-by-year tax impact at a 25% combined rate:

| Year | MACRS Deduction | Tax Savings | Cumulative Savings |

|---|---|---|---|

| 1 | $45,000 | $11,250 | $11,250 |

| 2 | $72,000 | $18,000 | $29,250 |

| 3 | $43,200 | $10,800 | $40,050 |

| 4 | $25,920 | $6,480 | $46,530 |

| 5 | $25,920 | $6,480 | $53,010 |

| 6 | $12,960 | $3,240 | $56,250 |

| Total | $225,000 | $56,250 | — |

After just two years, the company has recovered $29,250 in tax savings — more than half the total. Compare that to straight-line over 5 years: Year 1 and 2 combined would yield only $22,500 in savings. That $6,750 timing advantage can fund an extra van payment or cover maintenance costs. For tracking overall return on investment across your fleet, combine depreciation with revenue and operating cost data.

Depreciation Recapture: The Part Nobody Mentions Until You Sell

Depreciation isn't free money — it's a deferral. When you sell a depreciated asset for more than its book value, the IRS recaptures the depreciation as ordinary income (Section 1245 property) or at a special 25% rate (Section 1250 property for real estate).

Selling that $50,000 van for $15,000 after depreciating it to $0? You owe tax on the full $15,000 gain as ordinary income. If you used MACRS and your marginal rate is 25%, that's $3,750 in recapture tax. The net benefit of accelerated depreciation is the time value of the deductions you took early — you effectively got an interest-free loan from the IRS.

For real property held more than a year, depreciation recapture is capped at 25% regardless of your bracket. On a $400,000 building depreciated by $80,000 over 8 years, selling for the original $400,000 triggers $80,000 × 25% = $20,000 in recapture tax.

When This Calculator Gives Misleading Results

Intangible assets with indefinite lives

Goodwill, trademarks, and certain IP don't depreciate under standard methods. They're either amortized under Section 197 (15-year straight-line) or tested for impairment annually. This calculator doesn't handle amortization.

Mid-quarter convention applies

If more than 40% of your annual asset additions are placed in service in Q4, the IRS requires the mid-quarter convention instead of mid-year. This changes first-year and last-year percentages. Consult IRS Publication 946 or a tax professional for that scenario.

Listed property with mixed personal use

Vehicles, boats, and aircraft used partly for personal purposes face special depreciation limits. A $60,000 SUV used 70% for business can only depreciate $42,000 (the business portion). Luxury auto caps apply too — $20,200 maximum first-year deduction for passenger vehicles in 2024.

Pick the Right Method: A Decision Framework

Not sure which method fits your situation? Follow this logic:

Use MACRS (default for tax returns)

For any tangible business property placed in service after 1986. This is the IRS default — use it unless you have a specific reason not to. Combine with Section 179 or bonus depreciation for maximum first-year deductions.

Use Straight-Line (for GAAP financial statements)

Required for most financial reporting under US GAAP and IFRS. Also choose this for tax when you expect significantly higher income in future years and want to save deductions for higher-bracket years.

Use DDB or SYD (for internal management accounting)

When you need book depreciation that matches how the asset actually loses economic value. Technology and vehicles lose value fastest early — DDB mirrors that pattern better than straight-line for internal planning.