Why a 3.4% Bond Can Beat a 5% Bond

A tax-equivalent yield calculator settles an argument most investors get backwards: the bond with the bigger number on the label is not always the one that puts more money in your pocket. A tax-free municipal bond paying 3.4% can quietly out-earn a corporate bond paying 5% — because the muni’s coupon skips federal income tax, and often state tax too. The higher the tax bracket, the wider that gap grows. This page shows you the exact math, the point where munis stop winning, and the three mistakes that cost investors real money.

The myth

“A 5% bond always beats a 3.4% bond.” Investors compare the headline coupons and pick the bigger one.

The reality

In the 35% bracket with a 6% state tax, that 3.4% muni is worth a 6.16% taxable yield. It wins by a mile.

What Tax-Equivalent Yield Actually Measures

Tax-equivalent yield (TEY) is the pre-tax yield a taxable bond would need to leave you with the same take-home income as a tax-free bond. It puts two very different bonds on one honest scale. A Treasury or corporate bond hands you a coupon and then the IRS takes a cut of it every April. A qualified municipal bond hands you a coupon the federal government never touches — and if you live in the state that issued it, your state usually leaves it alone too. TEY translates that tax break into a number you can compare directly against any taxable bond, CD, or Treasury.

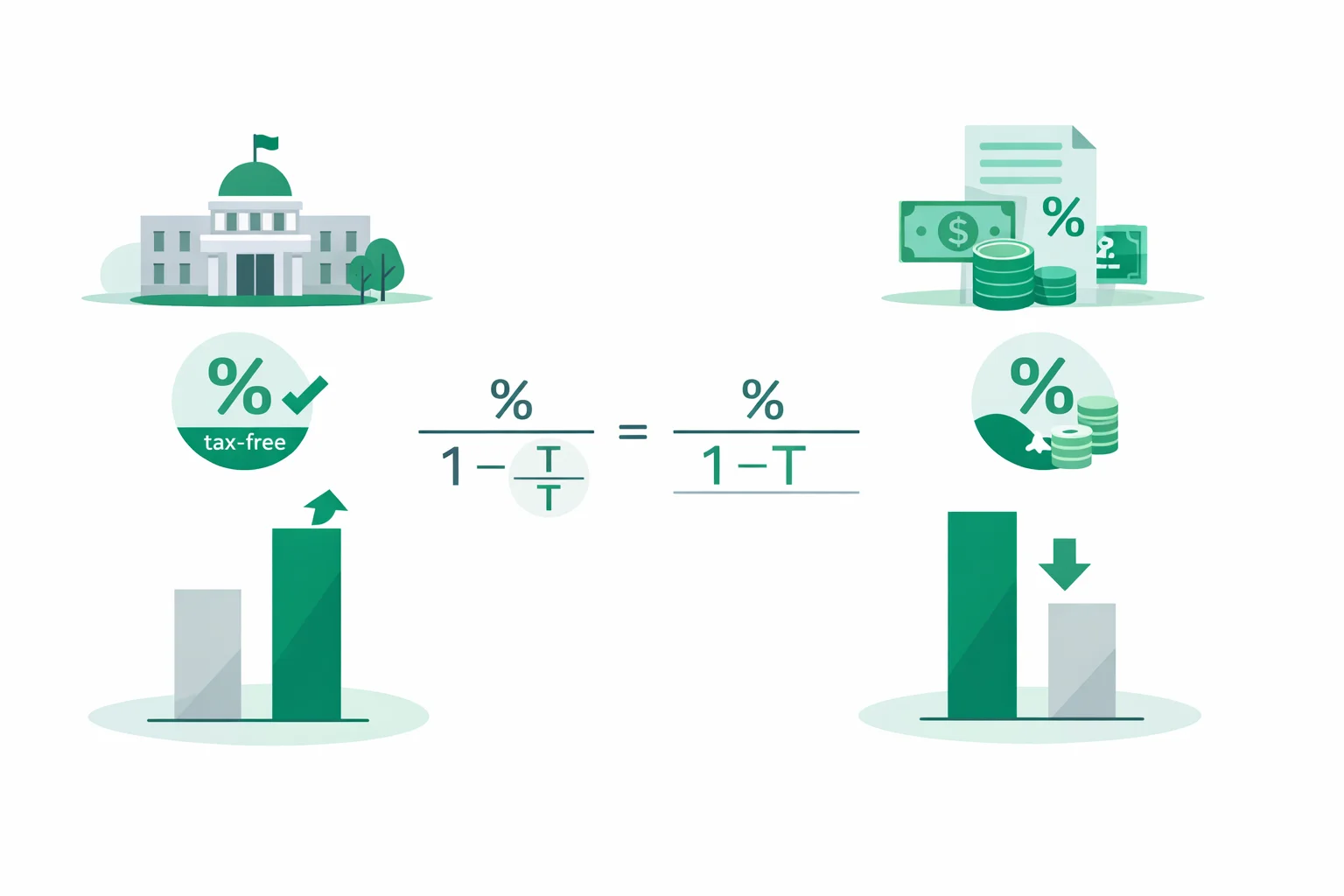

The Formula — and Why the Denominator Does the Work

The core formula is short, and the whole trick lives in the denominator:

Your combined tax rate stacks your federal marginal bracket, your state income tax rate, and — for higher earners — the 3.8% Net Investment Income Tax. Take a 3.4% in-state muni for someone in the 35% federal bracket with a 6% state rate who owes NIIT:

- Combined rate = 35% + 6% + 3.8% = 44.8%

- TEY = 3.4% ÷ (1 − 0.448) = 3.4% ÷ 0.552 = 6.16%

So that “small” 3.4% coupon is doing the work of a 6.16% taxable bond. Notice what drove the result: nothing in the numerator changed. The bigger your tax rate, the smaller the denominator, and the higher the equivalent yield climbs. This is the same after-tax logic behind an effective tax rate calculator — what matters is the money you keep, not the number on the statement.

How Much Does Your Tax Bracket Change the Answer?

Enormously. Below is the same 3.4% in-state muni measured against a 4.8% taxable bond, assuming a 5% state tax and no NIIT, across the federal brackets. Watch where the winner flips:

| Federal bracket | Combined rate | TEY of 3.4% muni | Winner vs 4.8% taxable |

|---|---|---|---|

| 12% | 17% | 4.10% | Taxable bond |

| 22% | 27% | 4.66% | Taxable bond |

| 24% | 29% | 4.79% | Roughly a tie |

| 32% | 37% | 5.40% | Municipal bond |

| 35% | 40% | 5.67% | Municipal bond |

| 37% | 42% | 5.86% | Municipal bond |

The crossover sits around the 24% bracket. If you’re in the 12% or 22% bracket, tax-free bonds usually give up too much yield to be worth it — you’re better off with a taxable bond, a Treasury, or a CD. Once you hit 32% and up, munis start to shine. This is exactly why municipal bonds are marketed to high earners and rarely to young investors in low brackets.

A Full Worked Example With Dollars, Not Just Percentages

Percentages are abstract, so put $250,000 to work. Sarah is in the 35% bracket, pays 6% state tax, and owes the 3.8% NIIT. She’s choosing between a 3.4% in-state muni and a 5.1% corporate bond.

- Muni: fully tax-free, so 3.4% × $250,000 = $8,500 a year, all kept.

- Corporate bond: 5.1% × $250,000 = $12,750 — but the 44.8% combined tax takes $5,712, leaving $7,038.

- The gap: the “lower-yielding” muni pays her $1,462 more every year. Over a decade, that’s about $14,600 in extra take-home income.

The corporate bond looked 1.7 percentage points richer on paper and still lost. That’s the entire point of running the numbers before you buy. If you also want to see how a bond’s price moves as rates change, pair this with a bond price calculator.

In-State vs Out-of-State: The State Tax Twist

Not every muni is fully tax-free to you. A bond issued by your own state is typically exempt from both federal and state tax. Buy a muni from another state and you usually still owe your home state’s income tax on the interest — which shrinks its advantage. On a 3.4% muni for a California resident paying 9.3% state tax, the in-state version keeps the full 3.4%, while an out-of-state version effectively drops to about 3.08% after state tax. In the calculator, un-check the “exempt from my state tax” box to see that haircut. If you live in a no-income-tax state like Texas or Florida, this distinction disappears — set your state rate to 0%.

Where the 3.8% NIIT Quietly Tips the Scales

The Net Investment Income Tax is the muni advantage most calculators forget. If your modified adjusted gross income tops roughly $200,000 (single) or $250,000 (married filing jointly), an extra 3.8% surtax lands on your taxable interest, dividends, and capital gains. Municipal bond interest is exempt from it. That 3.8% goes straight into your combined tax rate, and it makes the denominator smaller still. For a top-bracket investor, NIIT alone can push a 3.4% muni’s equivalent yield from 5.86% to well over 6%. Leaving it out understates how good munis are for exactly the people most likely to buy them.

Don’t Forget Treasuries Have Their Own Tax Break

Munis aren’t the only bonds with a tax angle. U.S. Treasury interest is fully taxable at the federal level but exempt from state and local income tax — the mirror image of a muni. So in a high-tax state, a Treasury quietly gets its own boost. A 4.5% Treasury for a California resident in the 9.3% state bracket has a state tax-equivalent yield of about 4.96%, because you skip the state tax that a comparable corporate bond would owe. When you compare three-way — muni, Treasury, and corporate — adjust each one for the taxes it actually escapes. Treat a Treasury like a fully taxable bond and you’ll understate it by 0.3–0.5 points in a high-tax state.

Common Mistakes That Cost Real Money

Using your average tax rate instead of your marginal rate. TEY runs on the rate applied to your nextdollar of income, not your blended effective rate. Plug in 22% when your marginal rate is 35% and you’ll understate a 3.4% muni’s equivalent yield by more than a full percentage point.

Ignoring state tax on out-of-state munis.Buying another state’s bond and assuming it’s fully tax-free can overstate your yield by 0.3–0.5 points in a high-tax state — enough to reverse the winner.

Holding munis in a Roth or IRA.Tax-advantaged accounts are already tax-free, so a muni wastes its superpower there. You give up yield for a tax break you don’t need — keep munis in taxable brokerage accounts.

When a Muni Is the Wrong Call

Tax-equivalent yield only tells half the story, and there are times the math points away from munis even when the TEY looks good:

- You’re in the 12% or 22% bracket. The tax break is too small to justify the lower coupon; a taxable bond or CD wins on take-home yield.

- The money is inside a 401(k), IRA, or Roth. There’s no tax to shelter, so reach for higher-yielding taxable bonds instead.

- You need every basis point of yield and can accept the tax. A retiree in a low bracket living off interest may simply want the bigger gross coupon.

- Credit risk isn’t priced in. TEY compares yields, not safety. A shaky high-yield muni and an investment-grade corporate aren’t the same bet, even at equal equivalent yields.

Choose Munis If, Choose Taxable If

Lean municipal if…

- You’re in the 32%, 35%, or 37% bracket

- You live in a high-tax state and can buy in-state bonds

- The money sits in a taxable account

- You owe the 3.8% NIIT

Lean taxable if…

- You’re in the 24% bracket or below

- You’re investing inside an IRA, 401(k), or Roth

- You live in a no-income-tax state and the muni is out-of-state

- A CD or Treasury offers a much higher gross yield

Tips for Getting an Accurate Comparison

Run the numbers with your realmarginal rate, not a round guess — a jump from the 32% to the 35% bracket changes a 3.4% muni’s equivalent yield by roughly 0.27 points. Compare bonds of similar maturity and credit quality, since a 2-year and a 20-year bond aren’t interchangeable. And when you’re weighing a muni against a bank CD, convert the CD’s rate the same way you would with an APY calculator so you’re comparing true annual returns, not stated rates. Small precision here compounds into hundreds of dollars a year on a six-figure position.

Bottom line:Don’t compare bond coupons directly. Convert the tax-free yield to its equivalent taxable yield first, then buy the one that leaves more in your account. For a 35%-bracket investor, a 3.4% muni beats anything taxable yielding less than 6.16%.