The $768 Question Every Interest-Only Borrower Faces

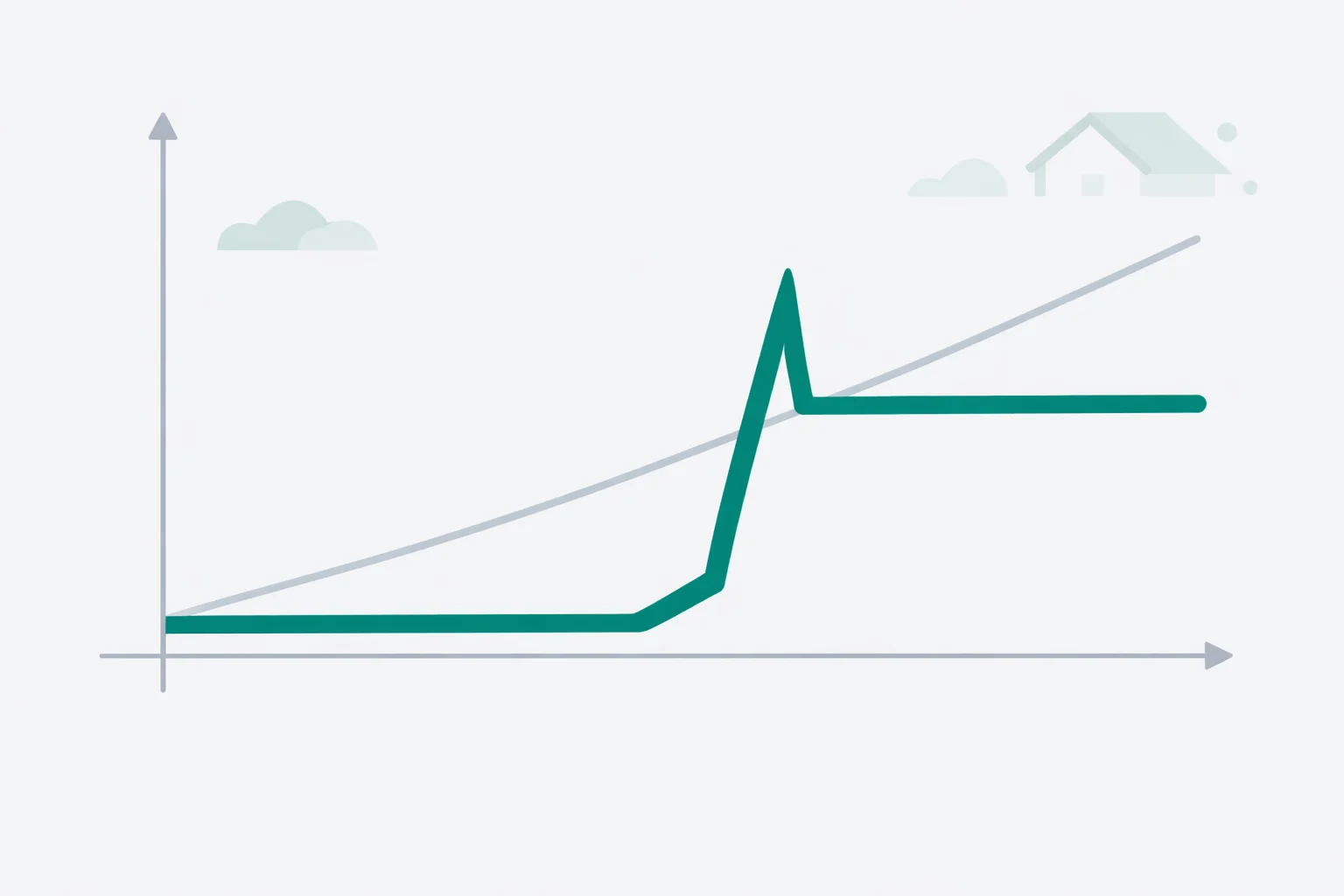

An interest-only mortgage calculator answers the one question that decides whether these loans are a smart tool or a trap: what happens to your payment when the interest-only period ends? On a $400,000 loan at 7%, you’d pay just $2,333 a monthfor the first 10 years — nothing but interest. Then in year 11 the payment recasts to $3,101, a $768 jump that lands in a single month, not gradually. That cliff is the entire story of an interest-only loan, and it’s exactly what the calculator above lets you see before you sign anything.

Lower payment now

You pay only the interest, so the monthly cost drops. On our example, $328 less per month than a standard loan — about $39,000 kept in your pocket over 10 years.

Bigger payment later

The full balance has to be repaid in the years that remain, so the payment jumps — often 30% to 50% overnight when the IO window closes.

More interest overall

Because you didn’t touch principal for years, total interest runs roughly $66,000 higher than the same loan paid the normal way.

What an Interest-Only Mortgage Actually Is

An interest-only mortgage lets you pay only the interest on your loan for a set opening stretch — usually 5, 7, or 10 years — while the principal sits completely untouched. Your balance on day 3,650 is identical to your balance on day one. When that period ends, the loan “recasts” and you begin paying both principal and interest, but compressed into the years that are left. A 30-year loan with a 10-year IO period gives you only 20 years to repay the whole balance, which is why the payment leaps.

Most interest-only loans today are also adjustable-rate, meaning the rate can move after a fixed window. That stacks a second variable on top of the recast — your payment can rise both because principal kicks inand because the rate resets. If your loan is an ARM, run the rate-reset side of the equation through an adjustable-rate mortgage calculator so you’re not blindsided by two jumps at once.

The Two Payments, and the Math Behind Each

An interest-only loan has two completely different payment formulas because it has two completely different phases. The interest-only payment is the simpler of the two — just the balance times the monthly rate:

On $400,000 at 7%, that’s $400,000 × (0.07 ÷ 12) = $2,333 a month. Every dollar goes to the lender as interest; the balance never budges. Once the IO period ends, the calculator switches to the standard amortization formula, but it only has the remaining term to work with:

Here P is still the full $400,000, r is the monthly rate (0.5833%), and n is the months left — 240, not 360. Plug those in and the payment comes to $3,101. Compare that to a normal 30-year loan on the same amount, which amortizes over all 360 months and costs $2,661 from the start. You can confirm that figure with a plain mortgage payment calculator. The interest-only loan is cheaper than the standard loan for 10 years, then more expensive for the next 20.

Why the Recast Hits So Hard

The payment shock isn’t a rate change — it’s a math change. During the IO years you were repaying $0 of a $400,000 balance. After the recast, that same $400,000 has to be gone in 20 years instead of the original 30. Squeezing the same debt into fewer years raises the payment even if your interest rate never moves an inch. That’s the trap borrowers miss: they assume a fixed rate means a stable payment, but the recast alone drives a 33% increase on our example loan. The bigger the balance and the shorter the remaining term, the harder the jump.

Interest-Only vs Standard: The Full 30-Year Picture

Side by side, the two loans trade places. The interest-only loan wins the first decade on cash flow and loses the next two on cost. Here’s how a $400,000 loan at 7% plays out both ways:

| Metric | Interest-only (10 yr IO) | Standard 30-year |

|---|---|---|

| Payment, years 1–10 | $2,333 | $2,661 |

| Payment, years 11–30 | $3,101 | $2,661 |

| Balance after 10 years | $400,000 | $343,000 |

| Total interest paid | $624,000 | $558,000 |

| Equity built by year 10 | $0 (from payments) | $57,000 |

The standard borrower has already knocked $57,000 off the balance by year 10. The interest-only borrower owes every penny of the original loan and pays $66,000 more in interest across the full term. To see exactly how principal and interest split apart month by month on the standard side, the mortgage amortization calculator maps the whole schedule.

Who Interest-Only Loans Genuinely Fit

These loans aren’t inherently bad — they’re a cash-flow tool that fits specific situations and burns everyone else. Use this framework to decide:

Interest-only can work if…

- Your income is lumpy — commissions or bonuses you’ll use to pay principal in chunks

- You’re a real estate investor maximizing monthly cash flow on a rental

- You’ll genuinely sell or refinance before the recast (a short, confirmed timeline)

- You invest the monthly savings at a return that beats your mortgage rate

It backfires if…

- You need the loan just to afford the house — the recast will break your budget

- You spend the monthly savings instead of investing them

- You’re counting on rising home values to bail you out

- You have no concrete exit plan before the IO window closes

The honest test: if the recast payment of $3,101 would strain your budget, you can’t actually afford this loan — you can only afford to delay it. Check the recast figure against the 28% rule using a home affordability calculator and qualify yourself on the higher payment, not the teaser one.

Mistakes That Turn a Tool Into a Trap

Spending the savings instead of investing them.The entire case for an IO loan is putting that $328 a month to work. Spend it, and you’ve simply paid $66,000 extra in interest for nothing.

Assuming you’ll refinance before the recast.Refinancing depends on your equity, credit, and rates you don’t control. If home values dip and you’ve built $0 in equity, you may be stuck with the full payment jump and no escape hatch.

Ignoring that IO rates run higher.Lenders price the added risk into the rate — typically 0.5% to 1% above a comparable standard loan. That premium eats into the cash-flow advantage before you even reach the recast.

When to Skip an Interest-Only Loan Entirely

For a primary residence you plan to keep long term, an interest-only mortgage usually costs more than it’s worth. You pay a higher rate, build no equity for years, and face a payment shock down the road — three strikes against a family that just wants a stable home. If your goal is simply a lower payment, extending the term or shopping the rate on a standard loan is safer. And if you want to tap equity you already have rather than skip principal on a purchase, an interest-only HELOC serves that need without restructuring your first mortgage. The one clear-cut case for an IO purchase loan is a disciplined investor or a borrower with a firm, near-term exit — everyone else is usually better served by a conventional loan.

What the Rules Require Lenders to Check

After the 2008 crash, interest-only loans nearly vanished, and the ones that came back are far more tightly regulated. Under the federal Ability-to-Repay rule, lenders generally must qualify you on the fully amortizing payment — the higher recast figure — not the low introductory one. That’s a consumer protection worth understanding: it means you legally can’t be approved for a payment you can’t sustain long term. Interest-only loans are also usually classified as “non-qualified” mortgages, which is why they often carry stricter down-payment and credit requirements. The Consumer Financial Protection Bureau spells out how these loans work and what to watch for before you commit.

Bottom line: run your real numbers through the calculator above, then qualify yourself on the recast payment, not the teaser. If $3,101 fits your budget and you have a plan for the monthly savings, an interest-only loan can be a sharp cash-flow tool. If it doesn’t, the calculator just saved you from a very expensive surprise in year 11.